Introduction

The problem of household over-indebtedness and the associated insolvency of households is one of the key contemporary challenges. With the introduction of the insolvency procedure into the national legal order, insolvent consumers have gained the chance to rid themselves of the ballast of debt.

From 1 December 2021, insolvency proceedings can be conducted remotely via the National Debt Register. This makes the proceedings significantly easier for indebted consumers, although the insolvent include individuals who are poor, affected by social and digital exclusion, lacking computer skills and sometimes even lacking access to appropriate hardware and the Internet.

The purpose of this article is to analyse the difficulties that digitally excluded people or those at risk of such exclusion may experience as claimants in insolvency proceedings. The main focus is on those who may be particularly at risk of poverty and exclusion from various areas of socio-economic activity, e.g. older people or single parents.

Methodology

The initial discussion focuses on the analysis of the phenomenon of digital exclusion based on the literature on the subject, especially in relation to vulnerable individuals, as well as statistical data showing the scale of financial exclusion collected by Eurostat and revealed in the ‘Fiberhost’ report. The next part of the article discusses the concept of personal bankruptcy based on a critical interpretation of legal acts, the literature on the subject and statistical data of the Ministry of Justice on personal bankruptcy, as well as information on the number of defaulters obtained from the database of debtors maintained by InfoDług BIG SA. The remainder of the paper contains key research, i.e. case studies based on interviews with ten debtors who have remotely filed for bankruptcy.

Review of the literature and statistics on the phe- nomenon of digital exclusion

In this part of the article, the discussion will mainly focus on issues related to the formation of the phenomenon of digital exclusion among people who are particularly at risk of over-indebtedness. People who are digitally excluded and over-indebted may also be at risk of other forms of exclusion, including social exclusion that involves preventing an individual from participating fully in socio-economic life, which is why the relationship between digital exclusion and other forms of marginalisation is also considered.

Technological progress is one of the most important factors in economic development. Thanks to the more widespread use of computers, then the Internet, productivity has increased among other things, and numerous innovations have emerged, bringing a number of benefits in both individual and macroeconomic terms. Digitalisation brings many benefits to poorer households, affecting their social inclusion and reducing poverty. However, not everyone is able to keep up with the rapidly changing realities and take advantage of new technologies. As a rule, higher economic growth is accompanied by higher levels of digitalisation of the economy and a lower risk of poverty and social exclusion (Kwilinski, Vyshnevskyi, Dzwigol, 2020).

Access to information has become one of the most important resources, and digital exclusion can lead to deep social divisions and inequalities (Popiołek, 2013). Rapid technological progress requires not only the possession of modern equipment, but also appropriate knowledge. Nowadays, those deprived of access to certain resources may experience many different difficulties in their normal socio-economic activities, which may lead to marginalisation (Kujawski, 2018). A digitally excluded person is deprived of opportunities for professional development, participation in the wider cultural life, as well as access to a variety of economic resources and the possibility to exercise a range of social and civil rights (Huczek, 2022).

The literature on the subject considers the problem of digital exclusion more broadly, i.e. it does not refer to the lack of physical access to IT technologies only, but also to the ability to use the achievements of civilisation, such as computers and the Internet. Two key types of determinants of digital exclusion can be distinguished, i.e. technological ones, resulting from the limited availability of hardware, software and access to infrastructure, and individual ones, which are varied and may be due to the lack of adequate knowledge, competence or motivation (Widawska et al., 2014).

According to Eurostat statistics, 93% of households in Poland had access to the Internet in 2022 (with the EU average at 92%) and this is an upward trend (Eurostat, 2022). However, in a more detailed study of the degree of digital inclusion (Digital Econony and Social Index, taking into account, inter alia, the level of social capital or Internet use), Poland ranked among the last in the EU, i.e. 25th (DENSI, 2022), although the number of people at risk of social exclusion has been decreasing in recent years while the level of digitisation remained low (Kwilinski, Vyshnevskyi, Dzwigol, 2020). Certain social groups are more at risk of digital exclusion, e.g. the elderly (55-74), which is due to the senior citizens’ health problems among other things as only 9.1% of the seniors with health complaints were using the Internet. (Czarnecka M. et al., 2023). According to the Fiberhost report, those most at risk of digital exclusion are seniors (55-74), poor households and rural residents (tab. 1). Therefore, the main determinants of digital exclusion in Poland are demographic (resulting from age), economic and geographical (Fiberhost. Digital Exclusion, 2022).

Table 1

Percentage of digitally excluded people (by main determinants of exclusion)

Digital exclusion entails a number of negative consequences in a wide range of socio-economic activities, limiting an individual’s access to various public and private resources such as the labour market, financial services or consumer goods. Digital exclusion is treated as one form of wider social exclusion, being a factor that exacerbates the marginalisation and isolation of the individual in an increasingly digital society (Czerski, 2020). Nowadays, a digitally excluded person is usually a socially excluded person as well, due to the significant impediments to everyday life resulting from a lack of access to IT (Garwol, 2019).

Digitally excluded people may also be deprived of the opportunity to deal with their affairs, including the privilege of debt relief during bankruptcy proceedings conducted through an online portal. The inability to rid themselves of the ballast of debt can expose insolvent individuals to a number of negative consequences, including poverty as a result of being deprived of part of their income and property assets as a result of various debt collection and enforcement actions. In addition, debtors may experience a number of other problems in different spheres of socio-economic life, e.g. difficulties in obtaining credit or restrictions in the use of bank accounts and transactional services. In extreme cases, insolvent individuals may take steps to evade debt collection by giving up legal work in favour of employment in the informal economy, which will deprive them of a number of entitlements (e.g. sickness benefits, access to public health services) and may expose them to even greater poverty and exacerbate their degree of social exclusion.

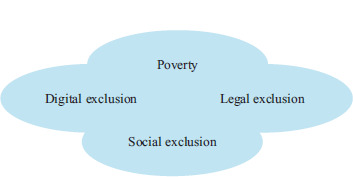

Figure 1

Relationship between poverty, digital exclusion, legal exclusion and social exclusion

Source: own study.

People who find it difficult to use new technical solutions for various reasons including health, e.g. the elderly or the disabled, are particularly at risk of digital exclusion (Kreft, 2012). This problem can also affect people with lower levels of education, the poor, or residents of smaller towns and villages where the Internet infrastructure is underdeveloped (Grześkowiak, 2014). The phenomenon of an ageing population in an era of increasing digitalisation of social life is also a major challenge as older people are at greater risk of digital exclusion (Adamczyk, Betlej, 2021).

Legal exclusion occurs when an individual has no access to certain entitlements, which can be due to external conditions (e.g. excessive costs) or to factors attributable to the excluded, usually resulting from their withdrawal from various aspects of social life (Staśkiewicz, 2010). Debtors may experience problems resulting from their difficult economic situation (e.g. lack of adequate facilities and Internet access) and from much more complex internal determinants due to the individual’s voluntary renunciation of the use of certain entitlements that would allow them to improve their economic condition, including debt relief procedures (Reczuch, 2013). Digital exclusion in conjunction with legal exclusion may violate the constitutional principle of equality (art.32(1) of the Constitution) by failing to ensure that every person has equal access to a fair trial (Kwiatkowska, 2023). The way in which certain spheres of life are regulated can encourage or discourage certain IT-enabled activities (Ułasiewicz, 2021).

Worse still, the areas of exclusion can overlap and thus reinforce their negative impact. Digital exclusion usually exacerbates social exclusion by restricting an individual’s access to a range of goods and also preventing them from exercising certain public rights (legal exclusion) and thus putting them at risk of deepening poverty.

Critical interpretation of the law, statistics and literature – the concept of personal bankruptcy in the national legal order

A restrictive version of personal bankruptcy was introduced on 31 March 2009 by way of the Act of 5 December 2008 amending the Bankruptcy and Reorganisation Law and the Act on costs in civil cases (Journal of Laws No. 234, item 1572). Subsequently, the law has been amended several times, facilitating access to this institution and introducing solutions to speed up the procedure. Important changes were introduced at the beginning of 2015 under the Act of 29 August 2014 amending the Bankruptcy and Reorganisation Law, the Act on the National Court Register and the Act on Court Costs in Civil Cases (Journal of Laws No. 1306 of 2014), which caused a rapid increase in the number of bankruptcies declared from 32 (in 2014) to 2,153 (in 2015). Another increase in the number of bankruptcies was due, among other things, to the subsequent amendment under the Act of 30 August 2019 amending the Bankruptcy Law and certain other acts (Journal of Laws of 2019, item 498), an essential part of which became effective as of 24

Table 2

Number of bankruptcy petitions filed, number of bankruptcies declared, percentage of bankruptcies declared in rela- tion to petitions filed, duration of bankruptcy proceedings and number of debtors between 2009 and 2022/

The next important amendment is effective as of 1 December 2021 and was introduced by the Act of 28 May 2021 amending the Act on the National Register of Debtors and certain other acts (Journal of Laws 2021.1080). The law makes it compulsory to submit letters via the National Register of Debtors portal, although there are a few exceptions, inter alia regarding consumers (Article 4912(3) in conjunction with Article 226a of the Bankruptcy Law). A natural person not acting as business entities can file a bankruptcy petition on paper, which will then be scanned and entered into the system by a court employee, which makes the procedure significantly easier for the digitally excluded, albeit exposing them to longer processing times than are the case for remote proceedings due to the submission of hardcopy documents.

Initially, bankruptcy cases were few and the average time taken to process bankruptcy petitions in 2009 was 2.1 months, with 985 cases received and only ten bankruptcies declared. Subsequently, the time taken to adjudicate cases more than doubled despite the simplifications and facilitations introduced to access the debt relief procedure.

There has been a steady increase in the proportion of people who have successfully declared bankruptcy since 2009. However, the data is incomplete as it only covers those petitions that have been successfully filed but not petitions from those unable to file remotely. The successive increase in the number of bankruptcies being declared is certainly a welcome result of the gradual streamlining of the procedure; however, several thousand petitions remain not granted.

It is also worth mentioning that the successive liberalisations of the bankruptcy law and further gradual easing of access to the debt relief procedure have not been able to reduce the increase in the number of insolvent individuals, which increased by more than 1 million between 2009 and 2018. Although there was a deceleration of this process between 2020 and 2021, this was probably mainly due to the deterioration of the economic situation of households during the COVID-19 pandemic and the avoidance of new financial commitments while facing an uncertain future and volatile macroeconomic environment.

Case studies

The case studies allow for an in-depth study of a small group of debtors who experienced various difficulties while using the National Debt Register portal. The results of these studies cannot be used to formulate general diagnoses, but they do allow for a thorough analysis of various anomalies. The applied case study methodology (face-to-face interviews consisting of conversations with the respondents) made it possible to analyse the circumstances presented by a small group of debtors (10). The interview had a semi-structured format, involving the collection basic information from the respondents (age, place of residence, education, family status), and then the respondents could describe, comprehensively and extensively, the problems arising from their insolvency and difficulties with debt removal using the remote procedure.

All of those interviewed initially filed for bankruptcy via the National Debt Register portal. All of those surveyed had access to the Internet and nine people also had e-mail addresses. Six people had their own computers and the rest used other people’s devices or used the Internet on mobile phones. Only one person had ePUAP, another had set up ePUAP for the purpose of these proceedings and the rest (8 people) submitted documents using electronic banking. It is worth adding that as many as nine of the respondents had bank accounts and, although they were usually seized in the course of enforcement proceedings, the respondents used them to send submissions among other things. Only one person used a lawyer (free advice) as the respondents did not have the financial means to hire a lawyer.

A 44 years’ old man, married, one adult child, former entrepreneur, university education, temporarily residing in Germany for work purposes, his place of residence in Poland was a medium-sized town (200,000 inhabitants) filed a petition himself at one of the smaller courts. The main problem was the debt resulting from the mortgage taken out to purchase real estate as the respondent was unable to repay it and also didn’t manage to sell the mortgaged property. Within about two weeks of filing, he received a notice to remedy formal deficiencies related to his previous business activities, which he completed by sending a first class letter (due to difficulties with the portal) and the bankruptcy was declared within about a month. The receiver contacted him by phone and this was how he learned about the court’s ruling as he did not keep up to date with the portal;

A 50 years’ old female, single, secondary education, working as a carer for the elderly in Germany, residing in a city of more than 500,000 inhabitants. Her debt amounted to several tens of thousands of zlotys (bank credits and loans) for current consumption, which she was unable to repay. Although she filed her petition electronically, a notice for particulars was sent in writing and delivered by post. The respondent struggled to provide the necessary information, which included the amount of her income, the submission of contracts related to her employment and information on her place of residence. She sent a letter to the court, which found the provided information to be incomplete and scheduled a hearing, after which it rejected the bankruptcy petition. The woman did not know the exact reasons for the court’s decision as she had not been present for the announcement of the ruling. She did not appeal or even request a statement of reasons for the final ruling as she had no knowledge of the appeal procedures;

A 48 years’ old female, married, secondary education, one adult child, working at Biedronka, living in a medium-sized city of 100,000 people. Financial management was the responsibility of her husband who took out loans for the business. The woman filed for bankruptcy herself and her husband still has not decided on this step, although he had planned to do so. The respondent filed the petition through the portal but was unable to complete it (quite a lot of information was missing, including the list of assets, the list of debts and bank statements). She completed the application on time but sent it by post (she did not know how to use the portal for this). However, the court returned her application and did not take into account the submission to make good formal deficiencies, which was delivered by post. Subsequently, the debtor filed another petition on paper, stating that she did not know how to use the portal and requested that correspondence be sent by post, although the court invited her to remedy the deficiencies again remotely;

A 34 years’ old female, secondary education, divorced and in a new relationship, mother of five children, residing in a city of more than 500,000 inhabitants. She had taken out several loans to finance the needs of her family, and was unable to repay them after the divorce. Her electronic petition required a number of additions, but the debtor did not keep track of the incoming e-mails and did not notice the message informing her of the deficiencies. She only realised that her petition had been returned after more than one year, when one of her creditors informed her of the fact. She filed another petition on paper and has been waiting for several months for it to be examined;

A 36 year’s old man, secondary education, in an informal relationship, father of one child, residing in a large city, i.e. over 500,000 inhabitants. He became insolvent due to one mortgage. His income diminished significantly during the COVID-19 pandemic while his loan instalments increased at the same time. He found out about the declared bankruptcy thanks to a phone call from the trustee, as there was no information about it on the portal, which he checked regularly;

A 28 years’ old debtor, secondary education, was in a cohabiting relationship, raising one child with the child’s mother, resided in a city with a population of more than half a million. He lost financial liquidity as a result of a few consumer loans and fell into what is known as a debt spiral, i.e. taking on more debt to repay previous loans. The money was used for various needs related to the birth of the child, including baptism, and furnishing the child’s room. The debtor filed the application shortly after the introduction of the remote procedure into the legal order. He had been checking the portal regularly for several months, but lost interest in his petition due to the lack of information (other than the assignment of the case number). The debtor subsequently forgot the password and no longer logged in. According to the publicly available information, his petition remained not considered after more than a year of submission;

A 70 years’ old pensioner, vocational education, married, two adult children, residing in a large city (over 500,000 inhabitants). The value of his debt is in the hundreds of thousands of zlotys and stems from his previous business activities back in the 1990s. The debtor had completely lost control of his indebtedness; he didn’t know the size of his debt and was even unable to identify all the creditors. It took him more than a year to assemble the documentation related to the debts. His son assisted in filing the petition through the portal (the respondent used his son’s e-mail address as he did not have an e-mail or a computer himself);

A 62 years’ old man, married, childless, vocational education, residing in a city with more than 500,000 inhabitants. He worked as a construction worker in the grey economy to protect his income from enforced debt collection. He was encouraged to declare bankruptcy by his wife, who had also previously declared bankruptcy (she did not use the portal). The debtor initially wanted to file the petition on paper and take it to the court himself, but was informed that new rules had been introduced, and the petition could only be filed via the portal. As the man did not have access to a computer, to the Internet, an e-mail address or a bank account, it took him more than two months just to file the petition (and, before that, to obtain ePUAP). The petition had quite a few formal deficiencies and, at his wife’s insistence, the debtor took advantage of the free assistance of a lawyer in remedying the formal deficiencies and declared bankruptcy;

A 45 years’ old man, secondary education, in the process of divorce, father of a disabled adult child, residing in a rural area. The debt resulted from one failed investment, i.e. the debtor acquired a cheap house to renovate it and run a workers’ hotel there, but was unable to repay the loan taken out for this purpose. The respondent hesitated for a very long time whether to file for bankruptcy, as this would have meant losing the property; he eventually filed the petition after his wife had filed for divorce, with the encouragement and help of a friend;

10. A 35 years’ old female, married, university education, two children, from a small town (20,000 inhabitants). The debt was incurred by her husband for his business – the respondent worked for her husband’s company as a shop assistant but did not have accurate knowledge of the debt, as the financial management was handled exclusively by her husband. She filed for bankruptcy several years earlier while the previous, more restrictive law was in force, but her petition was rejected. Another petition was filed in a court based in a town with a population of less than 100,000; it was heard within a month and the bankruptcy was declared;

Table 3

Proposed recommendations for state institutions and NGOs /

The problem of inclusion of digitally excluded people

Actions taken of public entities must lead to a reduction of digital exclusion both in technological, organisational and educational terms (Blażejewski, 2022). The aim of introducing various types of remote legal procedures is to make it easier for citizens to handle various matters, i.e. their social inclusion in legal and institutional terms. Insolvent individuals gain greater legal protection by having access to tools for quick and efficient debt relief. In the context of the analysed topic, the following determinants of inclusion for the digitally excluded can be distinguished:

The debt relief procedure should make it possible for cases to be dealt with efficiently and quickly online. Under the current rules, debtors initiating insolvency proceedings are required to provide a lot of data, for example, regarding their earnings, which could be added at a later stage of the proceedings, all the more so as the remedying of formal deficiencies poses a major challenge for respondents. A range of information could be obtained by the insolvency court ex officio, e.g. from debtors’ registers, which would streamline such proceedings. In addition, the centralised processing of applications by a single court, which would transfer the cases to the territorially competent district courts after the declaration of bankruptcy, could simplify and unify the practices of processing these applications, and reduce the time differences in their recognition between large metropolises and smaller towns (tab. 3).

Respective regulations should be linked to the creation of an easy-to-use, user-friendly portal that debtors can use intuitively, and educational elements should be introduced, i.e. pages containing more information should be added to the National Debtors Register. At present, information on consumer bankruptcy is scattered across many different sites and is too general to be of much help to petitioners for bankruptcy. Unfortunately, there is no coordinated system of legal aid and economic air for people experiencing problems due to over-indebtedness in Poland. In addition, the information on personal bankruptcy is not only vague, but also deals with procedural issues only, and purely legal knowledge should also be complemented by the information for the insolvent individuals on the management of personal finances in order to help them cope with the numerous challenges related to over-indebtedness. A proper response by households to the dangers of over-indebtedness requires in-depth economic and legal knowledge related to various ways of improving liquidity – bankruptcy must be seen as a last resort in this context. Access to knowledge in the broadest sense (not limited to instructions on how to use the portal) is one of the key pillars for building the information society and the modern economy.

In the light of quantitative statistical data, it is possible to hypothesise that, despite a gradual improvement in the economic standing of households and a decrease in poverty and social exclusion in Poland, there is still a high degree of digital exclusion measured according to the DENSI index (Kwilinski, Vyshnevskyi, Dzwigol, 2020). Previous research points to the complexity of digital exclusion in that, among other things, an improvement of the well-being of society and the development of digital technologies do not always automatically translate into a reduction of poverty or social exclusion. In addition, digital exclusion can exacerbate social exclusion in a number of different areas (Garwol, 2019) and promote the marginalisation of individuals (Czerski, 2020), including insolvent individuals who may be denied the chance of debt relief due to the lack of adequate skills, knowledge and flawed legal regulations.

During the case studies, people most at risk of poverty and social exclusion, e.g. the elderly or single parents, were deliberately selected for the research. While these figures are not representative, vulnerable individuals may be more prone to problems related to over-indebtedness and therefore more attention should be paid to such individuals due to the risk of deeper and more permanent social exclusion, one dimension of which is digital exclusion.

Summary

There is a fairly large and growing number of insolvent households in Poland. Successive legislative initiatives and amendments to the bankruptcy law have not been able to reduce the scale of this phenomenon, which is also due to the digital exclusion of debtors, a phenomenon that may be complex and multidimensional in the light of the case studies. Nowadays, remote procedures are a great help as they can significantly simplify the declaration of bankruptcy, but special solutions are required for this purpose that are going to take into account the socio- economic situation of insolvent individuals, with a particular focus on vulnerable individuals (e.g. the elderly). Current solutions, including the functionality of the National Register of Debtors portal, may be too difficult for at least some over-indebted individuals and prevent them from declaring bankruptcy. The existing legal regulations need to be changed, e.g. by facilitating the remedying of formal deficiencies, and above all, steps should be taken to integrate excluded people by expanding their knowledge. In turn, the creation of a comprehensive economic and legal counselling system addressed to the poor and the insolvent in particular, can significantly facilitate the fight against various types of exclusion from socio- economic life, including digital exclusion.